A natural extension of degree centrality is eigenvector centrality. In-degree centrality awards one centrality point for every link a node receives. But not all vertices are equivalent: some are more relevant than others, and, reasonably, endorsements from important nodes count more. The eigenvector centrality thesis reads:

A node is important if it is linked to by other important nodes.

Eigenvector centrality differs from in-degree centrality: a node receiving many links does not necessarily have a high eigenvector centrality (it might be that all linkers have low or null eigenvector centrality). Moreover, a node with high eigenvector centrality is not necessarily highly linked (the node might have few but important linkers).

Eigenvector centrality, regarded as a ranking measure, is a remarkably old method. Early pioneers of this technique are Wassily W. Leontief (The Structure of American Economy, 1919-1929. Harvard University Press, 1941) and John R. Seeley (The net of reciprocal influence: A problem in treating sociometric data. The Canadian Journal of Psychology, 1949).

The power method can be used to solve the eigenvector centrality problem. Let $m(v)$ denote the signed component of maximal magnitude of vector $v$. If there is more than one maximal component, let $m(v)$ be the first one. For instance, $m(-3,3,2) = -3$. Let $x^{(0)}$ be an arbitrary vector. For $k \geq 1$:

until the desired precision is achieved. It follows that $x^{(k)}$ converges to the dominant eigenvector of $A$ and $m(x^{(k)})$ converges to the dominant eigenvalue of $A$. If matrix $A$ is sparse, each vector-matrix product can be performed in linear time in the size of the graph.

The method converges when the dominant (largest) and the sub-dominant (second largest) eigenvalues of $A$, respectively denoted by $\lambda_1$ and $\lambda_2$, are separated, that is they are different in absolute value, hence when $|\lambda_1| > |\lambda_2|$. The rate of convergence is the rate at which $(\lambda_2 / \lambda_1)^k$ goes to $0$. Hence, if the sub-dominant eigenvalue is small compared to the dominant one, then the method quickly converges.

The built-in function evcent (R, C) computes eigenvector centrality.

A user-defined function eigenvector.centrality follows:

# Eigenvector centrality (direct method)

#INPUT

# g = graph

# t = precision

# OUTPUT

# A list with:

# vector = centrality vector

# value = eigenvalue

# iter = number of iterations

eigenvector.centrality = function(g, t) {

A = get.adjacency(g);

n = vcount(g);

x0 = rep(0, n);

x1 = rep(1/n, n);

eps = 1/10^t;

iter = 0;

while (sum(abs(x0 - x1)) > eps) {

x0 = x1;

x1 = as.vector(x1 %*% A);

m = x1[which.max(abs(x1))];

x1 = x1 / m;

iter = iter + 1;

}

return(list(vector = x1, value = m, iter = iter))

}

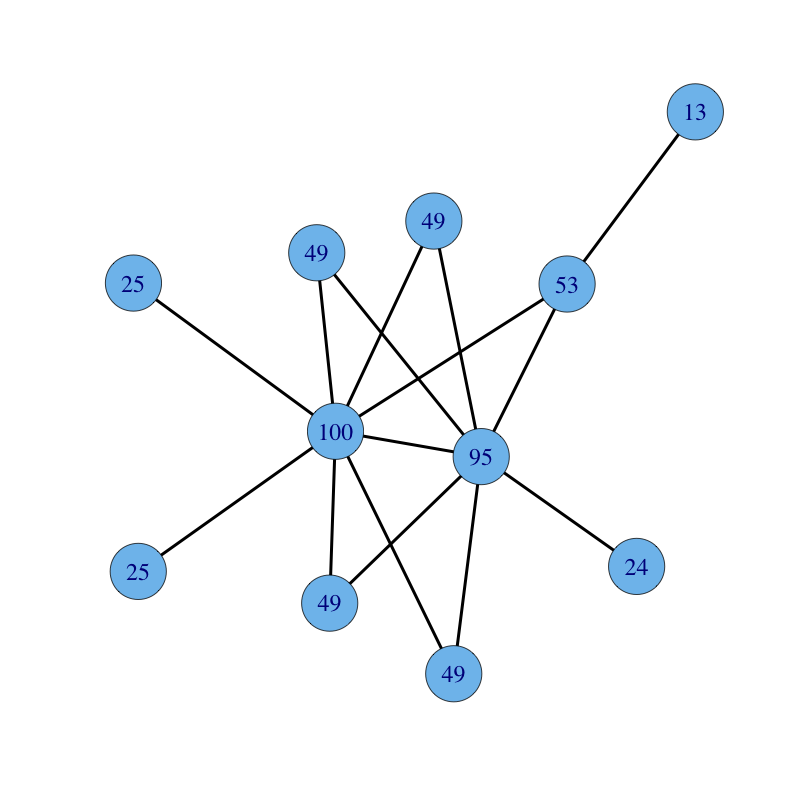

An undirected connected graph with nodes labelled with their eigenvector centrality follows: